Features

The convoluted LNG–NG story: What do we need? LNG or NG or neither?

By Eng. Parakrama Jayasinghe

parajaysinghe@gmail.com

I am not a fan of natural gas either in its gaseous state NG or the liquefied state LNG, both of which are very much under discussion now locally and at COP 26 in Glasgow. At the same time, I would like to consider myself a realist with the wellbeing and needs of Sri Lanka receiving the highest priority.

Natural gas, mostly Methane (CH4), is present in deep underground strata in large pockets or closer to the surface in a more dispersed manner, emanating from decaying biomass and also unfortunately emitted by ruminating bovine.

Those who enjoyed this natural but diminishing fossil fuel resource in their own territorial land mass or with access to neighbours in the same land mass could do so in it’s gaseous state, commence exploiting by laying extensive gas pipe lines sometimes running thousands of kilometres

But in recent decades , with larger volumes being discovered (with the USA and Canada exploiting environmentally disastrous tar sands and fracking practices), the lure of this seemingly economical and decidedly less polluting fossil fuel, has attracted even those countries not endowed with any indigenous gas resources on their own or neighbours with such resources accessible by pipelines. This has led to the development of the process of liquefaction of the NG by cooling down to about – 160 degrees under high pressure, purely for the purpose of economically acceptable logistics for transport mainly by sea, creating the LNG concept and market.

However, since NG can be used only in its gaseous form, at the recipient’s end re-gasification facilities are required and were implemented on land close to the point of use or in logistical distribution terminals. The oil and gas industry using their ingenuity came up with a further twist by development of the Floating Storage and Re Gasification Units (FSRU), designed to serve those who could not deploy the land based re-gasification facilities located on land as these could be quite expensive. As the name suggests, these are designed as floating vessels moored close to the point of use, and the LNG is delivered to the FSRUs by bulk NG carriers. The re-gasified NG is delivered in relatively short pipelines to the land based consumption units for example power plants.

This is decidedly a simple explanation for the understanding of laymen. There are extensive and detailed explanations given in several articles by Eng. Nalin Gunasekera, a renowned international expert on the subject, in the Daily News of 3, 4 and 5 November and the Sunday Island of 7 November 2021, for those interested in gaining a more in depth understanding of the issues associated with these systems.

However, my purpose in writing this comment is not to discuss such technical intricacies but to examine how Sri Lanka should evaluate the options and the best approach for our benefit if we are to consider either LNG or NG. As already mentioned, given the choice, I would not like having to use NG in any form. It is a fossil fuel and it is now recognised as a very significant contributor to Global Warming, being 80 times more potent than CO2 in the short term. But it has the advantage of being a cleaner burning fuel, devoid of a plethora of dangerous and toxic pollutants released to the entire exosphere.

What are Sri Lanka’s Options ?

Some important issues must be recognised prior to seeking a reply to this query. Viz:

We have now firmly established the target of 70% renewable energy contribution for power generation by 2030

The current forecasts the 30% contribution by fossil fuels in 2030 is 8997 GWh Vs the current contribution of 9000 GWh ( CEB 2020 statistics), which leaves no room for any additional fossil power plants, except as replacements for any due to be retired shortly. The 350 MW Sobhadhanawi plant can be justified only in this context.

The 900 MW Lak Vijaya coal power plant may have a residual economic life of about 25 years.

The price of coal has sky rocketed, reportedly to over $ 240 per ton at source and no suppliers even at that price to Sri Lanka

The price of crude oil too has shot up to $ 85 per BBL and seems to hold at that level.

As such, using NG to meet the 30% gap appears to be an option and environmentally less damaging at least at point of use, provided the cost of generation is acceptable.

The comparison between the CEB tender for the FSRU only, without considering the LNG supply cost and mechanism, with the NFE proposal, which includes a monopoly on supply of LNG at unknown prices, is most illogical and has no meaning, at all. Talk about comparing one rotten apple with an even more rotten orange.

In spite of the grave doubts cast by Eng. Nalin Gunesekera, there is a possibility of attracting investors to develop the Mannar gas resource due to reasons given later on

Where does that leave us? Have we no options at all?

To start with, there can be no justification to continue with this love affair with LNG, given that it will compel Sri Lanka to continue purchase of a fossil fuels with scarce Dollars and at prices on which we have absolutely no control. The attraction of $ 250 Million for the sale of a valuable national asset is no justification, however tight the present foreign exchange situation is, a hollow relief as it will result in draining out several billions of dollars in a few short years.

Next, an FSRU is an inevitable appendage to go with the LNG supplies. Eng. Gunasekera has gone to great lengths to explain the complexities of this system and the high degree of expenditure required for its implementation and operation as well as the great many risks involved in the whole deal. He comes from an expert with decades of experience in this sector, and we will indeed be fool hardy to ignore his warnings and fall into a trap, from which we have no escape.

The whole process of this attempt to get NG as an alternative source of fuel, without anyone competent, establishing the possible means of supply, and compounding the problem by awarding a contract for the construction of a power plant is laughable, if not for the tragic mess that has landed Sri Lanka in. This is even more tragic considering that there has been no in depth re-evaluation on financial and economic feasibility based on current supply and price issues, done before deciding to make an award for a project tendered for in 2016. Sri Lanka having painted itself into a corner, the solution is not to get blackmailed but to dump the LNG and FSRU options even at this late stage. It has been calculated by the SLSEA that even with the most optimistic assumptions on current prices of LNG the cost of generation with LNG will be of the order of Rs 35.00 per kWh. This can only go up with continued depreciation of the rupee and the price trends of the LNG.

Just for comparison, the Siyambaladuwa solar project is expected to generate electricity at Rs 11.00 per kWh and the Mannar Wind Plant is generating at less than Rs 10.00 per kWh. The current cost of adding batteries to make these firm sources of electricity generation is only Rs 8.50 per kWh and is expected to decline sharply in the coming years to Rs. 3.50 per kWh by 2025.

What about Yugadhanawi Power Plant and the supposed share sale of 40% shares to the New Fortress Energy ( NFE)? If this deal is already confirmed and the $ 250 Million is already received, then this share deal on its own would be carried out. But there cannot be any additional conditions such as a monopoly of supply of LNG, attached to this sale. Such conditions are totally illegal and we can only hope that the present litigation will support this point of view.

At present, the Yugadhanawi plant operates at about 30% plant factor. Let it continue to do so using the furnace oil, even though the cost of FO also may have gone up in recent times. The impact on the national economy and the CEB cash flow would be much less worrisome than the proposed misadventure with LNG.

What is the fate of Mannar Oil and Gas Resource?

Although Eng. Gunasekera is of the view that its proven potential is far too little to attract any investors, he has hedged his bets by a surprising comment on the possibility of this resource being supplementary to FSRU and LNG. Given the dire warnings he has sounded against any attempt to implement the FSRU, perhaps he may have an inkling that the Mannar resource may stand on its own.

However, I would like to take a more optimistic view of the possibility and the need for a successful development agreement (taking due notice of warnings given on this count too due to Sri Lanka’s poor record of international negotiations) for two reasons:

It is now becoming impossible to operate the Lak Vijaya coal power plant due to cost of coal.

We don’t seem to have the courage to look beyond the 70% RE target and therefore should look for a least damaging solution, both economically and environmentally.

Both these objectives are served by successful development of the Mannar gas field with the potential of gaining both more economically and financially as the estimated potential of 9 Trillion Cubic Feet of Gas from the currently explored blocks; this is many times our own potential consumption and will yield a substantial surplus.

The World Scene on Natural Gas

I must justify my claim to be a realist in hoping for an acceptable agreement for this development in spite of my opposition to any form of fossil fuels. The fact remains that it is only now that the CEB has accepted the 70% RE goal. So, we need to look for the least damaging means of meeting the balance 30%. In the world scene, in spite of the agreement that NG is a very potent GHG due to leakages at points of extraction, storage and transport, it remains a highly sought after fuel. While there is a widespread agreement to eventually end the use of coal, in some countries even as early as 2025, there is no such agreement in respect of NG.

Even at the current COP 26 summit dubbed as the Green Washing Festival by Greta Thunberg, the commitment is only to reduce the methane emissions by 30% by year 2030, that too with out several major producers and users of NG including India, Russia and China

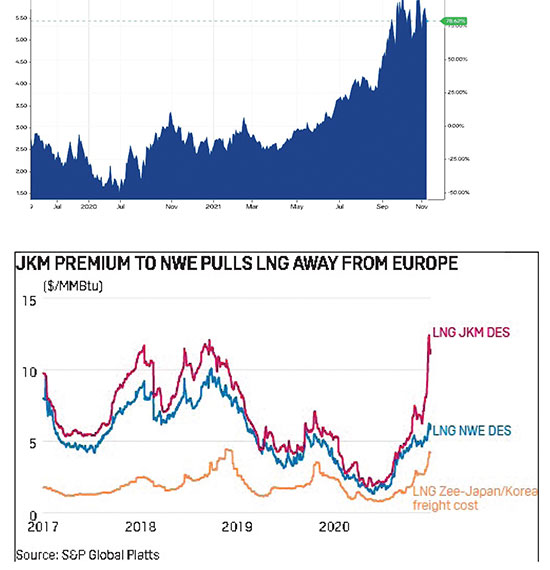

So, the demand and use of NG shall remain high and even escalate as replacement of coal in the foreseeable future. The largest increase is also expected to be in the Asian region. Coupled with this is the fact that there is a great gap between the quoted prices in different NG markets such as Henri Hub and the Japan Korea Market as shown in the graphs.

As such, developing our own resource is attractive and very much in centre stage of the high demand area.

So, while Sri Lanka has committed to reach Zero Carbon status by 2050, there is no reason why we should not aim at the least environmentally damaging and potential economically attractive option of opening up this resource as the transition solution.

The Worst Case Scenario?

What if we are not successful in getting an acceptable agreement and have to do without any gas?

This may be a reality considering the discussions going on at COP 26 against funding for any new fossil fuels. Many including me would view this as the best option in the long run.

Sri Lanka has enough and more indigenous RE resources and the 100% RE option is not impossible. The issue would be more of a financial problem than technical with the need for capital to import the necessary capital goods. There is hope generated at COP 26 on this count too. The project is already at the planning or implementation stage and such as the 100 MW solar and Wind Projects up to some 177 MW of major hydro projects would help bridge this gap in addition to the projected wind, biomass and solar potential .

The tantalising potential of doubling the generation capacity of the Victoria project on which feasibility studies have already been done needs urgent consideration.

Conclusion

The bottom line is clear. There are more than enough reasons for dumping the FSRU option before any more ill-considered commitments are made.

The possibility of attracting credible investors to develop the Mannar resource is reported to be very real and imminent. Therefore, a short sighted commitment to implement FSRUs and therefore the import of LNG would be most foolhardy.

There is the need for much more proactive measures to harness our own RE resources, not limiting such actions to mere rhetoric. The only ingredient lacking is the confidence as well as foresight of the energy authorities, blind to the world trends, both technically and commercially.

A time-targeted action plan towards the 70% RE is urgently needed with much greater emphasis on the next few years’ goals and activities. These would be invaluable in making adjustments to the plans for the next stage, say up to 2027. It is most likely that much more challenging targets could be set with the technical advances and the learning during the first stage.

Can we adopt this “Can Do” attitude at least now?