Business

The background to the International Sovereign Bond (ISB) settlement of USD 500 million on January 18, 2022

P.H.O. Chandrawansa, Former Controller of Exchange

The International Sovereign Bond settlement of USD 500 million on January 18, 2022, was routine and Parliament-approved budgeted debt repayment out of a total of approximately USD 7,100 million forex debt-servicing payments and Rs.3,000 billion local debt-servicing payments that were maturing in 2022.

According to published information, that amount of USD 500 million accounted for about 7% of the Government of Sri Lanka (Government) forex debt-servicing and about 2.3% of the total debt-servicing in 2022.

As per Section 113 of the Monetary Law Act, the Central Bank of Sri Lanka via its Public Debt Department (PDD) manages the public debt as the Agent of the Government. It is therefore the responsibility of the Government, and not the CBSL to borrow and to repay the Government Debt.

As the Agent, the Central Bank has to act on the direction and instructions of the Government in relation to public debt management and cannot unilaterally decide to pay or not to pay any debt of the Government. Further, it is the Government that makes funds available for local and foreign debt-servicing from the funds which have been specifically appropriated by Parliament for that purpose.

If, therefore for any reason, the Government were to decide to default on its debt repayments, that would have to be a decision of the Government. If the Government so decides, the Government, through the Ministry of Finance (MOF) must instruct the Central Bank not to re-pay any or all of the Government’s debts. Further, if such a far-reaching and vital decision were to be taken, it will obviously have to be the Government that would have to take the responsibility for the repercussions that would follow such a default as well.

The above position is clearly confirmed by the fact that it was the MOF that announced the new “Interim External Public Debt Servicing Policy” on April 12. 2022. Through the enunciation of that new policy, all forex debt repayments due to be settled by the Government up to that day, were to be stopped immediately, and restructured eventually. That announcement, inter alia, stated: “It shall therefore be the policy of the Sri Lankan Government to suspend normal debt servicing of All Affected debts (as defined below), for an interim period pending an orderly and consensual restructuring of those obligations in a manner consistent with an economic adjustment program supported by the IMF. The policy of the Government as discussed in this memorandum shall apply to amounts of Affected Debts outstanding on April 12, 2022. New credit facilities, and any amounts disbursed under existing credit facilities, after that date are not subject to this policy and shall be serviced normally”. The entire MOF statement is reported by Daily FT at : https://www.ft.lk/top-story/Sri-Lanka-declares-bankruptcy/26-733409

It should therefore be clear that until the above decision to default with effect from April 12, 2022 was taken by the Government, it was the bounden duty and responsibility of the Borrower (i.e, the Government) and its Agent (i.e, the Central Bank) to take all steps to honour the repayments of all Government debts falling due upto that date.

In addition, Finance Minister Basil Rajapaksa had also specifically given a clear re-assurance in Parliament about the repayment of the ISBs when winding up the Budget debate on December 10, 2021 (as reported in the Hansard page 2830) as follows: Translation: “Frankly, we facing a massive economic crisis. We are facing a foreign reserves crisis as well. However, as the Finance Minister, with the permission of the President and the Prime Minister, I must very solemnly confirm in this august assembly that we would pay every dollar that is due to be paid next year. I give that assurance with responsibility. First, we have to pay 500 million dollars in January. Next, we have to pay 1000 million dollars in July. In between, we have to pay other interest and capital repayments in our debt servicing. I hereby confirm to this august assembly that we will pay all that. We have a plan to do that. We will implement that plan”.

As is well known, when sovereign forex loans are not repaid, the credibility of the country will be lost. The country’s international credit rating will be slashed. Foreign direct investments and forex loans will be delayed. The country will probably lose access to international capital markets for many years. Local Banks will find it difficult to open letters of credit and carry out forex transactions. Forex funding of local banks will be curtailed by international lenders. Most forex-funded infrastructure projects will stop. Certain forex creditors will file legal action to recover their dues and the Government will incur huge litigation costs.

Some creditors may call for the re-structure of local debt, which, if done, could lead to serious socio-economic consequences. Thousands of small and medium sized businesses and entrepreneurs will face the risk of collapse. Hundreds of thousands of livelihoods will be in jeopardy. Inflation will escalate. Interest rates will rise sharply. Issue of Treasury Bills to the Central Bank (money printing) may increase significantly. The local currency will lose value. The Government’s local currency payments, including salary and pension payments, will be stressed.

It must therefore be appreciated that defaulting sovereign debt is a very complicated matter with grave consequences. It must also be understood that settling or not settling the country’s sovereign debt or a specific part of it, is not a matter where a single individual or even the CBSL can arbitrarily decide. Nevertheless, there have been claims by various persons and even some opposition MPs that the settlement of the maturing ISB of USD 500 million on January 18, 2022 was done at the behest of, and/or the sole discretion of then CBSL Governor Ajith Nivard Cabraal, in order to enable certain unspecified investors to make undue profits, ignoring the advice of various so called “experts”.

Ironically, when it was initially believed that the Sri Lankan Government may default on the January 2022 ISB, most of those so-called experts had previously warned about the grave consequences of default However, when it was subsequently known that the Government had secured the funds to settle the ISB, the same persons robustly and publicly advised sovereign default, and inexplicably found fault with the then Governor when their new amended “advice” to default was not heeded.

In that context, the bonafides of some of those persons would need to be questioned since they would have very well been aware that, as per the Offering Circular for the ISB of USD 500 million dated July 11, 2016, the Sri Lankan Government had solemnly assured all prospective investors of that Bond that, “the full faith and credit of the Democratic Socialist Republic of Sri Lanka will be pledged for the due and punctual payment of the principal of, and interest on, the Bonds.” Further the same persons would have also been aware that it is not possible to have selective defaults of particular sovereign loans, since many loan agreements with international creditors have “cross-default” clauses which are far-reaching.

In any event, at the time in question (January 2022), the official Government policy was to pay its sovereign debt, which policy, the MOF and the CBSL (as Agent) had followed faithfully and diligently, since independence. Needless to say, such deep-rooted policy could not, and should not have been unilaterally abrogated by the Governor and the Monetary Board of the CBSL on January 18, 2022, as lobbied by certain persons and politicians. It is therefore fortunate that the then Governor and Monetary Board did not listen to the unsolicited advice from those private individuals and politicians (who may have even been driven by various dubious agendas), as such advice should never have been acted upon by responsible state officials without a formal direction or official decision from the Government (the Borrower).

In fact, for argument’s sake, if the Governor and Monetary Board had, for some reason, not carried out the Government policy and defaulted on the payment of the ISB in January 2022, the same persons who are today vociferously finding fault with the former Governor for the payment of the ISB by the Government, would have probably castigated him and held him responsible for the calamitous outcomes that usually follow a sovereign debt default.

Accordingly, the Governors preceding the present Governor together the relevant CBSL staff must be commended for diligently following government policy and assisting the Government and MOF to settle its forex debt repayments during a highly stressful period. By doing so, they had assisted the Government to avoid irrevocable, permanent and catastrophic damage being inflicted upon the Sri Lankan economy.

The Delegation of German Industry and Commerce in Sri Lanka (AHK Sri Lanka) proudly facilitated the first-ever Sri Lankan delegation’s participation at Drupa 2024, the world’s largest trade fair for the printing industry and technology. Held after an eight-year hiatus, Drupa 2024 was a landmark event, marking significant advancements and opportunities in the global printing industry.

AHK Sri Lanka played a pivotal role in organising and supporting the delegation, which comprised 17 members from the Sri Lanka Association for Printers (SLAP), representing eight companies from the commercial, newspaper, stationery printing, and packaging industries. This pioneering effort by AHK Sri Lanka not only showcased the diverse capabilities of Sri Lanka’s printing sector but also facilitated vital bilateral discussions with key stakeholders from the German printing industry.

Business

Unveiling Ayugiri: Browns Hotels & Resorts sets the stage for a new era in luxury Ayurveda Wellness

In a captivating reimagining of luxury wellness tourism, Browns Hotels & Resorts proudly unveiled the exquisite Ayugiri Ayurveda Wellness Resort Sigiriya. This momentous occasion, celebrated amidst a vibrant and serene grand opening on the 6th of June, heralds a new chapter in the Ayurveda wellness tourism landscape in Sri Lanka. Nestled amidst 54 acres of unspoiled natural splendour, Ayugiri features 22 exclusive suites and stands out as the only luxury Ayurveda wellness resort in the country offering plunge pools in every room, rendering it truly one-of-a-kind.

The grand opening of Ayugiri Ayurveda Wellness Resort was an enchanting event, where guests were captivated by the melodies of flutists and violinists resonating through Sigiriya’s lush landscapes. As traditional drummers and dancers infused the air with vibrant energy, Browns Hotels & Resorts’ CEO, Eksath Wijeratne, Kotaro Katsuki, Acting Ambassador for the Embassy of Japan and General Manager, Buwaneka Bandara, unveiled the resort’s new logo, marking a significant moment witnessed by distinguished guests from the French Embassy, Ayurveda and wellness enthusiasts along with officials from the Sigiriya area, LOLC Holdings and Browns Group.

“Our strategic expansion into wellness tourism with Ayugiri Ayurveda Wellness Resort Sigiriya symbolises a significant milestone for Browns Hotels & Resorts. Wellness tourism has consistently outperformed the overall tourism industry for over a decade, reflecting a growing global interest in travel that goes beyond leisure to offer rejuvenation and holistic well-being. By integrating the timeless wisdom of Ayurveda with modern luxury, we aim to set a new standard in luxury wellness tourism in Sri Lanka. Whether your goal is prevention, healing, or a deeper connection to inner harmony, Ayugiri offers a sanctuary for holistic well-being” stated Eksath Wijeratne.

Ayugiri encapsulates the essence of life, inspired by the lotus flower held by the graceful queens of the infamous Sigiriya frescoes. Just as the lotus emerges from the murky depths, untainted and serene,

Ayugiri invites guests on a journey of purity and rejuvenation, harmonised with a balance of mind, body and spirit, the essence of nature, echoes of culture and the wisdom of ancient Ayurvedic healing.

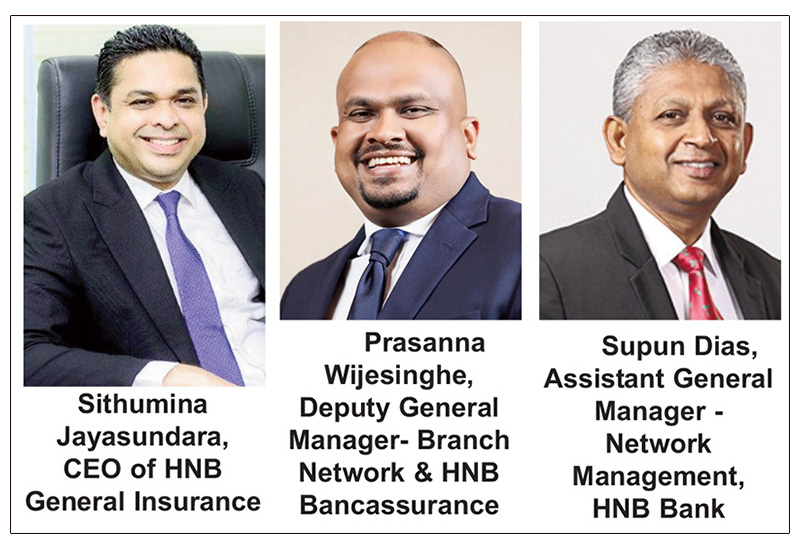

HNB General Insurance, one of Sri Lanka’s leading general insurance providers, has been honored as the Best General Bancassurance Provider in Sri Lanka 2024 by the prestigious Global Banking and Finance Review – UK.

The esteemed accolade underscores HNB General Insurance’s unwavering commitment to excellence and its outstanding performance in the field of bancassurance. Through dedication and hard work, the HNB General Insurance team has continuously endeavored to deliver innovative insurance solutions, cultivate strong relationships with banking partners, and provide unparalleled service to customers nationwide. This recognition is a testament to the team’s dedication and relentless pursuit of excellence in the bancassurance business.

“We are honored to receive this prestigious award, which reflects our team’s tireless efforts and dedication to delivering value-added insurance solutions and exceptional service through our bancassurance partnerships,” said Sithumina Jayasundara, CEO of HNB General Insurance. “This recognition reaffirms our position as a trusted insurance provider in Sri Lanka and motivates us to continue striving for excellence in serving our customers and communities.”

US sports envoys to Lanka to champion youth development

Rahuman questions sudden cancellation of leave of CEB employees