Features

Strengthening corporate governance: Rise of independent directors in audit committees

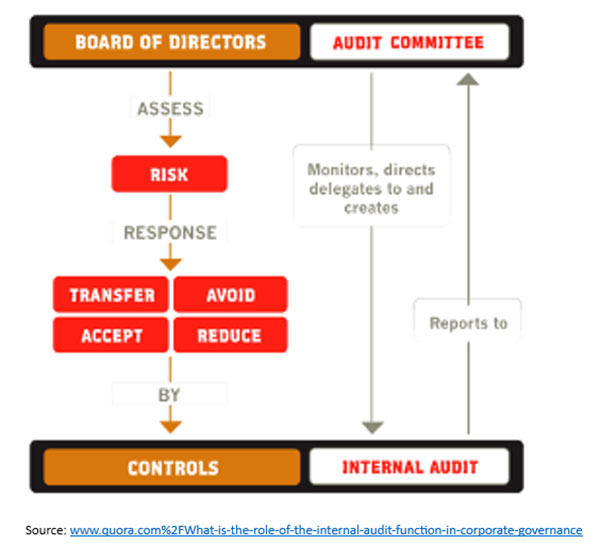

Corporate governance plays a critical role in ensuring transparency, accountability, and the protection of shareholders’ interests. In recent years, institutional investors in the United States have taken significant steps to enhance corporate governance practices, with a particular focus on the audit committee. (See Figure 01) One notable trend is the growing support for independent directors to lead audit committees. This essay explores the reasons for this shift, the benefits accruing therefrom to companies and shareholders, and the broader implications for corporate governance.

The Significance of Independent Directors:

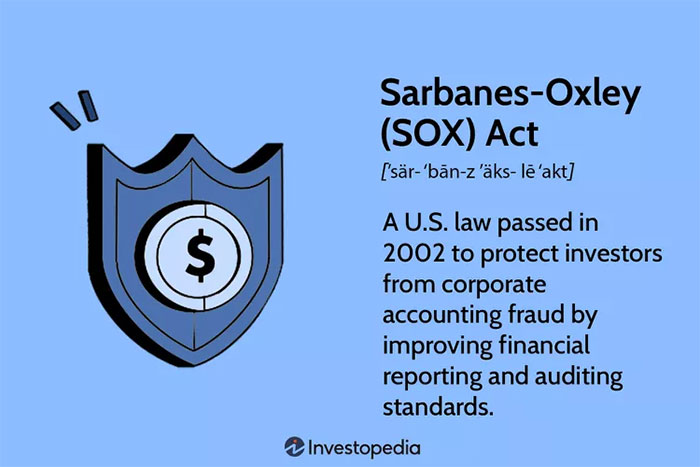

Under the Sarbanes-Oxley Act (SOX), the responsibilities of a firm’s board of directors have increased. (See Figure 02) This has led to a greater demand for professional directors who are solely focused on their board duties. Additionally, SOX has expanded the oversight role of the audit committee in ensuring the quality of financial reporting. To assess the effectiveness of audit committees, the relationship between professional directors on the audit committee and their monitoring capabilities is examined. Unexplained bad debt expenses are used as a measure of accounts receivable quality. The study finds that companies with a higher proportion of professional directors on their audit committees experience lower levels of unexplained bad debt expenses, indicating better accounts receivable quality. Furthermore, professional directors with accounting backgrounds on the audit committee directly contribute to reducing unexplained bad debt expenses and improving accounts receivable quality. Additionally, the positive effects of professional directors on unexplained bad debt expenses are enhanced when there is greater information asymmetry present.

Independent directors are individuals who have no material relationship with the company, its management, or its major shareholders. As impartial overseers, they are well-positioned to provide unbiased and objective perspectives on the company’s financial reporting and internal controls. The inclusion of independent directors in key roles, such as the audit committee, aims to mitigate conflicts of interest and ensure the integrity of financial reporting processes.

Role of the Audit Committee and Investors’ Advocacy:

The audit committee is an essential component of corporate governance, responsible for overseeing the financial reporting process, internal controls, and the external audit. This committee acts as a safeguard against financial misconduct, ensuring compliance with accounting standards, and maintaining the accuracy and reliability of financial statements.

Institutional investors, such as pension funds, mutual funds, and asset management firms, hold substantial stakes in numerous companies. Their collective influence gives them a strong voice in shaping corporate policies and practices. In recent times, these investors have increasingly supported the appointment of independent directors to chair audit committees, viewing it as a strategic move to strengthen corporate governance and protect shareholder interests.

There is a growing trend that institutional investors prefer to appoint professionally qualified university professors as independent to corporate board which they control. These professors are accustomed to critically analyzing information, challenging assumptions, and considering multiple viewpoints. Their objectivity is crucial in evaluating proposals, assessing risks, and ensuring decisions are made in the best interest of the company and its stakeholders. Their impartiality enhances board discussions and minimizes the risk of biases or conflicts of interest.

Reasons for Voting Independent Directors to Head Audit Committees:

Unbiased Oversight: Independent directors bring an external perspective, free from any conflicts of interest or undue influence from company management. This impartiality ensures that the audit committee’s decisions are solely based on the best interests of the company and its shareholders.

Enhanced Financial Oversight:

Independent directors possess expertise in finance, accounting, and auditing. Their professional backgrounds equip them to assess financial statements critically and engage effectively with auditors, enabling robust financial oversight.

Improved Investor Confidence: The presence of independent directors at the helm of audit committees sends a positive signal to investors. It signifies a commitment to transparency and ethical practices, fostering investor trust and confidence in the company’s operations.

Regulatory Compliance: Corporate governance guidelines, such as those provided by stock exchanges and regulatory bodies, often recommend the inclusion of independent directors in audit committees. By complying with these guidelines, companies demonstrate their commitment to meeting industry standards and regulations.

Risk Management: Independent directors’ focus on risk assessment and mitigation can help companies identify and address potential financial risks promptly. This proactive approach safeguards the company against potential crises and enhances long-term sustainability.

Increasing support from institutional investors for independent directors to head audit committees reflects a broader push towards stronger corporate governance practices in the United States. By embracing impartial oversight, companies can improve financial reporting, enhance investor confidence, and strengthen their overall risk management strategies.

Independent directors play a vital role in ensuring that the audit committee operates with the utmost integrity and professionalism. Their unbiased perspectives and expertise in finance and auditing bolster the committee’s effectiveness in safeguarding shareholder interests and promoting transparent financial practices. As the business landscape continues to evolve, the role of independent directors in corporate governance is likely to become even more pivotal in maintaining trust, integrity, and accountability within companies.

In addition to the advantages of professionally qualified university professors, the influence of independent directors on share prices has also received much attention.

While limited empirical research specifically explores the correlation between independent directors with finance specialization, particularly finance professors, and share prices, existing studies indirectly support the notion that finance specialized independent directors can influence share prices through their expertise in financial analysis, valuation, and capital allocation. The presence of independent directors on boards is seen as crucial in corporate governance, providing checks and balances in decision-making processes. Their specialized knowledge can positively impact firm performance, financial reporting quality, and investor confidence.

These findings highlight the significance of including professionals with substantial industry experience and finance specialization on corporate boards. Their expertise contributes to informed decision-making, risk management, and strategic oversight. Additionally, the influence of independent directors on share prices emphasizes the importance of corporate governance and the potential impact of board composition on firm performance and investor perception. Further research is warranted to establish a direct correlation between finance specialized independent directors and share prices, providing deeper insights into the role of independent directors in enhancing shareholder value and corporate governance practices.

As organizations strive for effective governance, these research findings offer valuable guidance for board composition and the selection of qualified professionals who can contribute to sound decision-making, enhance financial performance, and align with shareholder interests. The recognition of the benefits brought by professionals with industry experience and finance specialization paves the way for more inclusive and knowledgeable boardrooms, strengthening corporate governance practices across industries.

(The author, a senior Chartered Accountant and professional banker, holds a PhD from AUT university in New Zealand. He has authored numerous national and international publications. Currently, he is Professor in Business Management at SLIIT Business School, SLIIT University, Malabe. The views and opinions expressed in this article are solely those of the author and do not necessarily reflect the official policy or position of the institution he works for.)