Features

Purchasing Power Parity

by Kumar David

Why is the Russian economy not crumbling despite sanctions? In an analysis carried in Quora.com French economist Jacques Sapir wrote: ‘The reason for this miscalculation is exchange rates. If you simply convert Russia’s GDP from rubbles to dollars, you see it as an economy only as large as Spain’s. However, such comparisons are spurious without adjusting for Purchasing Power Parity (PPP) which accounts for productivity and living standards, and thus per capita welfare and resource use. In fact, PPP is the preferred metric of most international institutions from the IMF to the OECD.

Note by this columnist. [A very good plate of rice and curry for a worker costs Rs 600 in Sri Lanka, that is about US$1.62 at the official exchange rate of Rs 370 to the US$. But you cannot get an equivalent meal at that price in the US; it will cost at least $5. But if you take the exchange rate as Rs 120 to the US$ you get $5 for your Rs 600. Therefore, the PPP exchange rate is Rs 120 to one US dollar, not Rs 370 to a dollar].

When you measure Russia’s, GDP based on purchasing power parity it is like Germany’s in size; Russia about $4.4 trillion versus Germany $4.6 trillion. From a small sickly-looking economy to the largest European and one of the largest in the world, this is not a comparison that can be ignored. Sapir also encourages us to ask: “What is the share of production and industry compared to services?” In his view, today’s services sector is grossly overvalued compared to industries and commodities such as oil, gas, copper and agricultural commodities. If we deduct the role of services as a proportion of the global economy, Sapir says, “Russia’s economy is much bigger than Germany’s, maybe five or six percent of the world economy”, more like Japan’s.

This makes intuitive sense. When times are tough we know it’s more valuable to provide people with the things they need, like food and energy, than intangible things like entertainment or financial services. When a company like Netflix trades at a price-to-earnings ratio three times higher than Nestle, the world’s largest food company, that is a reflection of frothy markets not reality. Netflix is a great service company, but when 800 million people in the world are undernourished Nestle offers more value. The current Ukrainian crisis helps clarify why what were regard as “archaic” parts of the modern economy, such as industry and commodities whose prices have soared this year are more important than overvalued services and “technology” companies whose values have declined recently.

The scope an economy is further distorted by ignoring global trade flows, of which Mr Sapir estimates Russia “may account for 15 per cent”. For example, while Russia is not the world’s largest oil producer, it is the largest oil exporter, surpassing even Saudi Arabia. The same is true of many other basic products, such as wheat, the world’s most important food crop, of which Russia controls about 19.5 per cent of global exports, as well as nickel (20.4 per cent), semi-finished iron (18.8 per cent), platinum (16.6 per cent) and frozen fish (11.2 per cent). Such an important position in the production of so many basic commodities means that Russia, along with several other similarly placed countries are linchpins in the global production chain. Maximum sanctions” on countries like Iran or Venezuela trying to cut Russia of world markets are phoney and likely bring about rearrangement of the global economy to the disadvantage of the West.

Much of this has been proved by the war in Ukraine. Controlling oil, gas, food and other commodities, the war of sanctions waged by the United States and its Allies in Europe and Asia has become a headache for the West. Corroborating this view JPMorgan says Russia’s economy is stronger than expected and will only suffer a shallow recession despite sanctions. The Wall Street bank said business sentiment surveys from the country “are signalling a not very deep recession in Russia and therefore imply an ‘upside risk’ to our growth forecasts.

The Russian economy has so far fared better than expected under tough sanctions and is likely to suffer only a shallow but drawn-out recession according to JPMorgan. The bank told clients last week that the country’s economy is in better shape than expected, judging from business surveys and indicators such as electricity consumption and financial flows. “The data at hand therefore does not point to an abrupt plunge in activity at least for now. GDP in the second quarter would likely be better than predicted in March”.

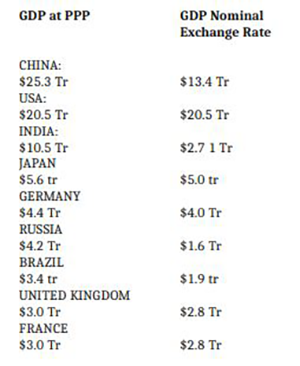

Purchasing power parity (PPP) is the rate of currency conversion that equalises the purchasing power of different countries by eliminating differences in price levels of essential goods. According to this concept two currencies are in equilibrium—known as the currencies being at par—when a basket of goods is priced the same in both countries taking into account the said PPP exchange rates. The importance of this point is emphasised in the Table below and has significant implications for Sri Lanka.

GDP by Purchasing Power Parity vs Nominal GDP

GDP by PPP which is based on a basket of goods is a fairer comparison between countries. In the table below Tr stands for trillions of US$.

Source: International Monetary Fund

The difference is very big in the case of countries outside the global capitalist market system. In the case of India GDP in PPP terms is an astounding 3.87 times (10.5/2.71) larger than the conventional GDP. This is a bit of a paradox because India is visibly very poor so where is all the wealth hiding? The answer lies in the huge disparity of wealth and income between the filthy rich and the dirt poor. This disparity in India is much larger than the disparity between the top 10% (or 1%) and the average person in the US.

I am not smart enough nor adequately statistically well informed to make anything but broad generalisations about Sri Lanka. My view is that; (a) in terms of living standards the true exchange rate is about Rs 120 (not Rs 370) to a US$, (b) the importance of domestic finance-capital (investment and mutual funds etc.) should be heavily discounted in policy decisions, (c) the hard-core productive sectors must be given far more attention and (d) other productive sectors like SMEs and the informal economy must be supported far more than now.

These economic factors will play out through the political dimension. Ranil Wickremesinghe (RW) has made himself a pariah in the eyes of every strand of democratic and liberal opinion, the diplomatic community in Colombo and international human and democratic rights movements. The Catholic Church is known for conservatism, when its Cardinal sees the RW and the previous government as cussed curs what more is there for anyone of us to say?

Concurrently Batalanda Ranil, his other avatar, has unleashed his military on protestors, journalists (local and foreign), reappointed alleged human rights violators in the Defence Ministry and deployed unlawful goon squads. Reactionaries in the State machine have trapped him into a spiral of violence. Ranil blundered when he played his Batalanda card for a second time; his baton wielding goons spared neither protestor nor public. Meanwhile the Mahinda clan which cut a path to the top for RW, basks in their billion-rupee (or $?) sunshine. Ranil must be criticised mercilessly till he is compelled to reverse course on democratic rights. He may then be able to chug along as a compromise president.

We the people have to exercise the utmost vigilance till Ranil is house-tamed and he has capitulated on the danger he poses to a free society. An early election will clear the decks of a lot of crap and let the people know where every political actor and party stands. After that the country can decide how it will adjust to inevitable belt-tightening (we have consumed for 70 years without producing the equivalent) and decide how to deal with our internal fiscal deficit and our foreign account indebtedness. The two are intimately interconnected; we do not have two problems but one tightly interconnected problem.

And there is the related matter of how much to relax exchange controls in order to attract FDI and capital flows. This is in the face of the 10-year Treasury Bond yield exceeding 25% at this moment and interest rates having to be correspondingly high. The IMF has demanded Central Bank independence, it has also demanded future debt sustainability and wants China on board for a haircut. These are tough issues to be addressed in this column in their own right at another time.

Ranil has decided to fly a kite about turning Sri Lanka into a Social (sic!) – he seems unaware that the accepted usage is ‘Socialist’ – Market Economy. What on earth is a “Social Economy” anyway? Does he appreciate what he is pontificating? I have been long engaged with the topic and published a paper in the Hector Abhayavardhana 80th birthday celebration volume issued in year 2000. After 22 years it still remains relevant and can be purchased from Marshal Fernando’s Ecumenical Institute on Havelock Road.