Features

Comparative Analysis of Global Monetary Policies and Economic Trends

This essay delves into the recent developments in global monetary policies, interest rates, and economic outlook. It synthesises information from various sources, including predictions of the end of the rate-hike cycle, unexpected decisions by central banks and the impact on emerging markets. Additionally, it contrasts these trends with the rapid economic recovery in the US., shedding light on the interconnectedness of global economies.

End of Rate Hike Cycle and Future Policy Expectations

The Reserve Bank of Australia (RBA) decided to hike its cash rate by 25 basis points to 4.35% in November 2023, a 12-year high. The increase, widely anticipated by economists, was the central bank’s 13th rate rise since May 2022. Meanwhile, the Governing Council of the European Central Bank (ECB) decided to raise the three key ECB interest rates by 25 basis points to 4.00% – 4.75%, with effect from 20 September 2023.

The Reserve Bank of Australia (RBA) decided to hike its cash rate by 25 basis points to 4.35% in November 2023, a 12-year high. The increase, widely anticipated by economists, was the central bank’s 13th rate rise since May 2022. Meanwhile, the Governing Council of the European Central Bank (ECB) decided to raise the three key ECB interest rates by 25 basis points to 4.00% – 4.75%, with effect from 20 September 2023.

It reflects a consensus among major central banks, including the Federal Reserve (Fed) in USA, Reserve Bank of New Zealand and Bank of England (BoE), etc., to conclude the rate hike cycle due to anticipated economic slowdowns and lower inflation by the end of the year. The expected strategy involves maintaining high policy rates until mid-2024, followed by possible rate cuts to counter falling inflation and an overall restrictive monetary policy until the end of 2024.

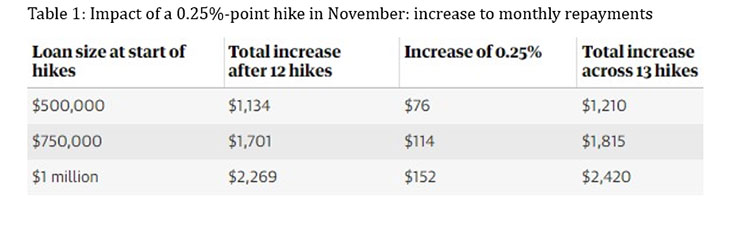

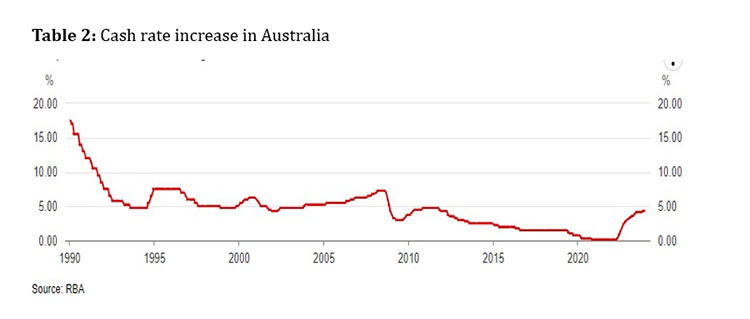

The consequences of a 0.25% (25 basis points) increment are clearly depicted in Table 1, indicating an impact of $152 for every 25 basis points on a home loan of $1 million. Beginning in late 2022, the consecutive series of 13 hikes has led to a significant ninefold escalation, resulting in a total increase of approximately $1,368. This escalation presents a substantial challenge for individuals relying on wages and carrying mortgages, particularly since this trend commenced in 2021 when the prevailing interest rate was only 0.1% (refer to Table 2), effectively doubling the repayment obligations.

An unexpected move by the ECB saw it raising rates for the 10th consecutive time. The decision was surrounded by uncertainties, balancing arguments for and against further hikes. This unexpected move contrasts with the decisions of the Fed and BoE, opting for a status quo in September.

An unexpected move by the ECB saw it raising rates for the 10th consecutive time. The decision was surrounded by uncertainties, balancing arguments for and against further hikes. This unexpected move contrasts with the decisions of the Fed and BoE, opting for a status quo in September.

Inflation Outlook and Monetary Policy Response

The prediction suggests that overall inflation in the European Union is expected to be around 3% by year-end, notably lower than the peak in Q4 2022. Despite this, core inflation is expected to decrease less, leading the ECB to keep its restrictive policy rates until mid-2024. This strategy aligns with a dedication to combat inflation and shows a careful approach compared to more optimistic growth predictions.

In September 2023, around 10 out of 40 central banks raised their policy rates, including the ECB. This marks a departure from the global tightening trend that began in 2021, with the ECB’s decision to continue rate hikes standing out.

The Bank of Japan (BoJ) is expected to tighten in April 2024, potentially diverging from the Fed, ECB, RBA and BoE, which might continue rate hikes based on their degree of monetary restraint.

Policy Rate Scenario and Duration

Many economists support a “high for long” position, expecting policy rates to remain at their current high levels for eight months (from October 2023 to May 2024) for the Fed, ECB, and BoE. Rate cuts are envisioned from mid-2024 in response to falling inflation, with the Fed and BoE considering regular cuts and the ECB adopting a more gradual approach.

Skepticism surrounds the optimistic economic outlook, with some economists expressing a belief that the U.S. may not avoid a recession due to tighter monetary policy. The anticipated shallow nature of the recession might give the impression of a “soft landing” despite challenges.

Global Impact on Emerging Markets

The quick economic recovery in the U.S., propelled by a fast vaccine rollout and a large fiscal stimulus, led to a notable rise in longer-term U.S. interest rates. This has sparked worries among emerging economies, dealing with a slower recovery due to delayed vaccine distribution and limited fiscal support. The impact on emerging markets hinges on the reasons behind the rise in U.S. interest rates. Positive news about U.S. jobs or COVID-19 vaccines tends to attract portfolio inflows, while a rise driven by expectations of more hawkish central bank actions can lead to capital outflows, currency depreciation, and increased spreads on U.S. dollar-denominated debt.

In emerging markets, a 10 percent rise in the value of the US dollar (DXY= US $ Index), influenced by global financial markets, leads to a 1.9 percent reduction in economic output after one year. This impact persists for two and a half years. In advanced economies, the negative effects are much smaller, reaching a peak of 0.6 percent after one quarter and largely disappearing within a year.

Sri Lanka is at the forefront of this trend, primarily because of mismanagement of reserves and the long-term pegging followed by a sudden shift to floating, contrary to the IMF’s advice. This stance was emphasized by the Supreme Court in its groundbreaking judgment on November 14, 2023.

Monetary Policy Surprises and Market Responses

A rise in U.S. interest rates due to expectations of more hawkish central bank actions can harm emerging market economies. Each percentage point increase in U.S. interest rates triggered by “monetary policy surprises” tends to result in immediate capital outflows from emerging markets, currency depreciation, and higher spreads on dollar-denominated debt.

The current increase in U.S. interest rates is attributed mainly to positive economic prospects, but factors such as a rising term premium contribute to uncertainty. Some advanced economy interest rates are still low, with the potential for further increases, raising concerns about the fragility of emerging market economies.

Policy Recommendations for Emerging Markets

To navigate the challenges posed by higher global interest rates, economists suggest that emerging markets should adopt accommodative monetary policies at home. Recommendations include lengthening debt maturities, limiting currency mismatches, and enhancing financial resilience.

As a precautionary measure, emerging market economies are advised to take steps to boost financial resilience. They underscore the importance of strengthening the global financial safety net through arrangements like swap lines and multilateral lenders. The International Monetary Fund’s precautionary financial facilities and a new allocation of special drawing rights are highlighted as tools to enhance member countries’ buffers against financial volatility.

Conclusion

In summary, the world economy faces diverse monetary policies, different rate outlooks, and uncertainties about the future. The complex interplay of major central banks, its effects on emerging markets, and the suggested strategies highlight the intricate dynamics of the interconnected global economy. As central banks address inflation, economic rebound, and possible risks, clear communication, flexibility, and global collaboration are crucial for maintaining a stable and robust global financial system.

(The writer, a senior Chartered Accountant and professional banker, is Professor at SLIIT University, Malabe. He is also the author of the “Doing Social Research and Publishing Results”, a Springer publication (Singapore), and “Samaja Gaveshakaya (in Sinhala). The views and opinions expressed in this article are solely those of the author and do not necessarily reflect the official policy or position of the institution he works for.)

by Dr Gotabhya Ranasinghe

Senior Consultant Cardiologist

National Hospital Sri Lanka

When we sought a meeting with Hon Dr. Ramesh Pathirana, Minister of Health, he graciously cleared his busy schedule to accommodate us. Renowned for his attentive listening and deep understanding, Minister Pathirana is dedicated to advancing the health sector. His openness and transparency exemplify the qualities of an exemplary politician and minister.

Dr. Palitha Mahipala, the current Health Secretary, demonstrates both commendable enthusiasm and unwavering support. This combination of attributes makes him a highly compatible colleague for the esteemed Minister of Health.

Our discussion centered on a project that has been in the works for the past 30 years, one that no other minister had managed to advance.

Minister Pathirana, however, recognized the project’s significance and its potential to revolutionize care for heart patients.

The project involves the construction of a state-of-the-art facility at the premises of the National Hospital Colombo. The project’s location within the premises of the National Hospital underscores its importance and relevance to the healthcare infrastructure of the nation.

This facility will include a cardiology building and a tertiary care center, equipped with the latest technology to handle and treat all types of heart-related conditions and surgeries.

Securing funding was a major milestone for this initiative. Minister Pathirana successfully obtained approval for a $40 billion loan from the Asian Development Bank. With the funding in place, the foundation stone is scheduled to be laid in September this year, and construction will begin in January 2025.

This project guarantees a consistent and uninterrupted supply of stents and related medications for heart patients. As a result, patients will have timely access to essential medical supplies during their treatment and recovery. By securing these critical resources, the project aims to enhance patient outcomes, minimize treatment delays, and maintain the highest standards of cardiac care.

Upon its fruition, this monumental building will serve as a beacon of hope and healing, symbolizing the unwavering dedication to improving patient outcomes and fostering a healthier society.We anticipate a future marked by significant progress and positive outcomes in Sri Lanka’s cardiovascular treatment landscape within the foreseeable timeframe.

by Fr. Emmanuel Fernando, OMI

Jesuit Fr. Aloysius Pieris (affectionately called Fr. Aloy) celebrated his 90th birthday on April 9, 2024 and I, as the editor of our Oblate Journal, THE MISSIONARY OBLATE had gone to press by that time. Immediately I decided to publish an article, appreciating the untiring selfless services he continues to offer for inter-Faith dialogue, the renewal of the Catholic Church, his concern for the poor and the suffering Sri Lankan masses and to me, the present writer.

It was in 1988, when I was appointed Director of the Oblate Scholastics at Ampitiya by the then Oblate Provincial Fr. Anselm Silva, that I came to know Fr. Aloy more closely. Knowing well his expertise in matters spiritual, theological, Indological and pastoral, and with the collaborative spirit of my companion-formators, our Oblate Scholastics were sent to Tulana, the Research and Encounter Centre, Kelaniya, of which he is the Founder-Director, for ‘exposure-programmes’ on matters spiritual, biblical, theological and pastoral. Some of these dimensions according to my view and that of my companion-formators, were not available at the National Seminary, Ampitiya.

Ever since that time, our Oblate formators/ accompaniers at the Oblate Scholasticate, Ampitiya , have continued to send our Oblate Scholastics to Tulana Centre for deepening their insights and convictions regarding matters needed to serve the people in today’s context. Fr. Aloy also had tried very enthusiastically with the Oblate team headed by Frs. Oswald Firth and Clement Waidyasekara to begin a Theologate, directed by the Religious Congregations in Sri Lanka, for the contextual formation/ accompaniment of their members. It should very well be a desired goal of the Leaders / Provincials of the Religious Congregations.

Besides being a formator/accompanier at the Oblate Scholasticate, I was entrusted also with the task of editing and publishing our Oblate journal, ‘The Missionary Oblate’. To maintain the quality of the journal I continue to depend on Fr. Aloy for his thought-provoking and stimulating articles on Biblical Spirituality, Biblical Theology and Ecclesiology. I am very grateful to him for his generous assistance. Of late, his writings on renewal of the Church, initiated by Pope St. John XX111 and continued by Pope Francis through the Synodal path, published in our Oblate journal, enable our readers to focus their attention also on the needed renewal in the Catholic Church in Sri Lanka. Fr. Aloy appreciated very much the Synodal path adopted by the Jesuit Pope Francis for the renewal of the Church, rooted very much on prayerful discernment. In my Religious and presbyteral life, Fr.Aloy continues to be my spiritual animator / guide and ongoing formator / acccompanier.

Fr. Aloysius Pieris, BA Hons (Lond), LPh (SHC, India), STL (PFT, Naples), PhD (SLU/VC), ThD (Tilburg), D.Ltt (KU), has been one of the eminent Asian theologians well recognized internationally and one who has lectured and held visiting chairs in many universities both in the West and in the East. Many members of Religious Congregations from Asian countries have benefited from his lectures and guidance in the East Asian Pastoral Institute (EAPI) in Manila, Philippines. He had been a Theologian consulted by the Federation of Asian Bishops’ Conferences for many years. During his professorship at the Gregorian University in Rome, he was called to be a member of a special group of advisers on other religions consulted by Pope Paul VI.

Fr. Aloy is the author of more than 30 books and well over 500 Research Papers. Some of his books and articles have been translated and published in several countries. Among those books, one can find the following: 1) The Genesis of an Asian Theology of Liberation (An Autobiographical Excursus on the Art of Theologising in Asia, 2) An Asian Theology of Liberation, 3) Providential Timeliness of Vatican 11 (a long-overdue halt to a scandalous millennium, 4) Give Vatican 11 a chance, 5) Leadership in the Church, 6) Relishing our faith in working for justice (Themes for study and discussion), 7) A Message meant mainly, not exclusively for Jesuits (Background information necessary for helping Francis renew the Church), 8) Lent in Lanka (Reflections and Resolutions, 9) Love meets wisdom (A Christian Experience of Buddhism, 10) Fire and Water 11) God’s Reign for God’s poor, 12) Our Unhiddden Agenda (How we Jesuits work, pray and form our men). He is also the Editor of two journals, Vagdevi, Journal of Religious Reflection and Dialogue, New Series.

Fr. Aloy has a BA in Pali and Sanskrit from the University of London and a Ph.D in Buddhist Philosophy from the University of Sri Lankan, Vidyodaya Campus. On Nov. 23, 2019, he was awarded the prestigious honorary Doctorate of Literature (D.Litt) by the Chancellor of the University of Kelaniya, the Most Venerable Welamitiyawe Dharmakirthi Sri Kusala Dhamma Thera.

Fr. Aloy continues to be a promoter of Gospel values and virtues. Justice as a constitutive dimension of love and social concern for the downtrodden masses are very much noted in his life and work. He had very much appreciated the commitment of the late Fr. Joseph (Joe) Fernando, the National Director of the Social and Economic Centre (SEDEC) for the poor.

In Sri Lanka, a few religious Congregations – the Good Shepherd Sisters, the Christian Brothers, the Marist Brothers and the Oblates – have invited him to animate their members especially during their Provincial Congresses, Chapters and International Conferences. The mainline Christian Churches also have sought his advice and followed his seminars. I, for one, regret very much, that the Sri Lankan authorities of the Catholic Church –today’s Hierarchy—- have not sought Fr.

Aloy’s expertise for the renewal of the Catholic Church in Sri Lanka and thus have not benefited from the immense store of wisdom and insight that he can offer to our local Church while the Sri Lankan bishops who governed the Catholic church in the immediate aftermath of the Second Vatican Council (Edmund Fernando OMI, Anthony de Saram, Leo Nanayakkara OSB, Frank Marcus Fernando, Paul Perera,) visited him and consulted him on many matters. Among the Tamil Bishops, Bishop Rayappu Joseph was keeping close contact with him and Bishop J. Deogupillai hosted him and his team visiting him after the horrible Black July massacre of Tamils.

Sri Lanka-Singapore Free Trade Agreement

By Gomi Senadhira

senadhiragomi@gmail.com

“You might tell fairy tales, but the progress of a country cannot be achieved through such narratives. A country cannot be developed by making false promises. The country moved backward because of the electoral promises made by political parties throughout time. We have witnessed that the ultimate result of this is the country becoming bankrupt. Unfortunately, many segments of the population have not come to realize this yet.” – President Ranil Wickremesinghe, 2024 Budget speech

Any Sri Lankan would agree with the above words of President Wickremesinghe on the false promises our politicians and officials make and the fairy tales they narrate which bankrupted this country. So, to understand this, let’s look at one such fairy tale with lots of false promises; Ranil Wickremesinghe’s greatest achievement in the area of international trade and investment promotion during the Yahapalana period, Sri Lanka-Singapore Free Trade Agreement (SLSFTA).

It is appropriate and timely to do it now as Finance Minister Wickremesinghe has just presented to parliament a bill on the National Policy on Economic Transformation which includes the establishment of an Office for International Trade and the Sri Lanka Institute of Economics and International Trade.

Was SLSFTA a “Cleverly negotiated Free Trade Agreement” as stated by the (former) Minister of Development Strategies and International Trade Malik Samarawickrama during the Parliamentary Debate on the SLSFTA in July 2018, or a colossal blunder covered up with lies, false promises, and fairy tales? After SLSFTA was signed there were a number of fairy tales published on this agreement by the Ministry of Development Strategies and International, Institute of Policy Studies, and others.

However, for this article, I would like to limit my comments to the speech by Minister Samarawickrama during the Parliamentary Debate, and the two most important areas in the agreement which were covered up with lies, fairy tales, and false promises, namely: revenue loss for Sri Lanka and Investment from Singapore. On the other important area, “Waste products dumping” I do not want to comment here as I have written extensively on the issue.

1. The revenue loss

During the Parliamentary Debate in July 2018, Minister Samarawickrama stated “…. let me reiterate that this FTA with Singapore has been very cleverly negotiated by us…. The liberalisation programme under this FTA has been carefully designed to have the least impact on domestic industry and revenue collection. We have included all revenue sensitive items in the negative list of items which will not be subject to removal of tariff. Therefore, 97.8% revenue from Customs duty is protected. Our tariff liberalisation will take place over a period of 12-15 years! In fact, the revenue earned through tariffs on goods imported from Singapore last year was Rs. 35 billion.

The revenue loss for over the next 15 years due to the FTA is only Rs. 733 million– which when annualised, on average, is just Rs. 51 million. That is just 0.14% per year! So anyone who claims the Singapore FTA causes revenue loss to the Government cannot do basic arithmetic! Mr. Speaker, in conclusion, I call on my fellow members of this House – don’t mislead the public with baseless criticism that is not grounded in facts. Don’t look at petty politics and use these issues for your own political survival.”

I was surprised to read the minister’s speech because an article published in January 2018 in “The Straits Times“, based on information released by the Singaporean Negotiators stated, “…. With the FTA, tariff savings for Singapore exports are estimated to hit $10 million annually“.

As the annual tariff savings (that is the revenue loss for Sri Lanka) calculated by the Singaporean Negotiators, Singaporean $ 10 million (Sri Lankan rupees 1,200 million in 2018) was way above the rupees’ 733 million revenue loss for 15 years estimated by the Sri Lankan negotiators, it was clear to any observer that one of the parties to the agreement had not done the basic arithmetic!

Six years later, according to a report published by “The Morning” newspaper, speaking at the Committee on Public Finance (COPF) on 7th May 2024, Mr Samarawickrama’s chief trade negotiator K.J. Weerasinghehad had admitted “…. that forecasted revenue loss for the Government of Sri Lanka through the Singapore FTA is Rs. 450 million in 2023 and Rs. 1.3 billion in 2024.”

If these numbers are correct, as tariff liberalisation under the SLSFTA has just started, we will pass Rs 2 billion very soon. Then, the question is how Sri Lanka’s trade negotiators made such a colossal blunder. Didn’t they do their basic arithmetic? If they didn’t know how to do basic arithmetic they should have at least done their basic readings. For example, the headline of the article published in The Straits Times in January 2018 was “Singapore, Sri Lanka sign FTA, annual savings of $10m expected”.

Anyway, as Sri Lanka’s chief negotiator reiterated at the COPF meeting that “…. since 99% of the tariffs in Singapore have zero rates of duty, Sri Lanka has agreed on 80% tariff liberalisation over a period of 15 years while expecting Singapore investments to address the imbalance in trade,” let’s turn towards investment.

Investment from Singapore

In July 2018, speaking during the Parliamentary Debate on the FTA this is what Minister Malik Samarawickrama stated on investment from Singapore, “Already, thanks to this FTA, in just the past two-and-a-half months since the agreement came into effect we have received a proposal from Singapore for investment amounting to $ 14.8 billion in an oil refinery for export of petroleum products. In addition, we have proposals for a steel manufacturing plant for exports ($ 1 billion investment), flour milling plant ($ 50 million), sugar refinery ($ 200 million). This adds up to more than $ 16.05 billion in the pipeline on these projects alone.

And all of these projects will create thousands of more jobs for our people. In principle approval has already been granted by the BOI and the investors are awaiting the release of land the environmental approvals to commence the project.

I request the Opposition and those with vested interests to change their narrow-minded thinking and join us to develop our country. We must always look at what is best for the whole community, not just the few who may oppose. We owe it to our people to courageously take decisions that will change their lives for the better.”

According to the media report I quoted earlier, speaking at the Committee on Public Finance (COPF) Chief Negotiator Weerasinghe has admitted that Sri Lanka was not happy with overall Singapore investments that have come in the past few years in return for the trade liberalisation under the Singapore-Sri Lanka Free Trade Agreement. He has added that between 2021 and 2023 the total investment from Singapore had been around $162 million!

What happened to those projects worth $16 billion negotiated, thanks to the SLSFTA, in just the two-and-a-half months after the agreement came into effect and approved by the BOI? I do not know about the steel manufacturing plant for exports ($ 1 billion investment), flour milling plant ($ 50 million) and sugar refinery ($ 200 million).

However, story of the multibillion-dollar investment in the Petroleum Refinery unfolded in a manner that would qualify it as the best fairy tale with false promises presented by our politicians and the officials, prior to 2019 elections.

Though many Sri Lankans got to know, through the media which repeatedly highlighted a plethora of issues surrounding the project and the questionable credentials of the Singaporean investor, the construction work on the Mirrijiwela Oil Refinery along with the cement factory began on the24th of March 2019 with a bang and Minister Ranil Wickremesinghe and his ministers along with the foreign and local dignitaries laid the foundation stones.

That was few months before the 2019 Presidential elections. Inaugurating the construction work Prime Minister Ranil Wickremesinghe said the projects will create thousands of job opportunities in the area and surrounding districts.

The oil refinery, which was to be built over 200 acres of land, with the capacity to refine 200,000 barrels of crude oil per day, was to generate US$7 billion of exports and create 1,500 direct and 3,000 indirect jobs. The construction of the refinery was to be completed in 44 months. Four years later, in August 2023 the Cabinet of Ministers approved the proposal presented by President Ranil Wickremesinghe to cancel the agreement with the investors of the refinery as the project has not been implemented! Can they explain to the country how much money was wasted to produce that fairy tale?

It is obvious that the President, ministers, and officials had made huge blunders and had deliberately misled the public and the parliament on the revenue loss and potential investment from SLSFTA with fairy tales and false promises.

As the president himself said, a country cannot be developed by making false promises or with fairy tales and these false promises and fairy tales had bankrupted the country. “Unfortunately, many segments of the population have not come to realize this yet”.

(The writer, a specialist and an activist on trade and development issues . )

US sports envoys to Lanka to champion youth development

Rahuman questions sudden cancellation of leave of CEB employees